Impact of Interest Rates on the Private Credit Space

Co-authored by Alan Rios, and Jairo Ortiz

Introduction

Interest rates play a critical role in the financial ecosystem, influencing borrowing costs, investment decisions, and overall economic growth. For private credit companies like Stratus Financial, understanding the dynamics of interest rates is crucial to managing risk and optimizing returns. This white paper provides an in-depth analysis of interest rate trends, rate risk, and their impact on private credit markets.

HISTORICAL CONTEXT AND CURRENT TRENDS

Historical Perspective

Interest rates in the United States have experienced significant fluctuations over the past few decades. Post the 2008 financial crisis, the Federal Reserve adopted a near-zero interest rate policy to stimulate economic recovery. This low-rate environment persisted for several years, fostering favorable conditions for borrowing and investment in various asset classes, including private credit.

Recent Developments from the Federal Reserve

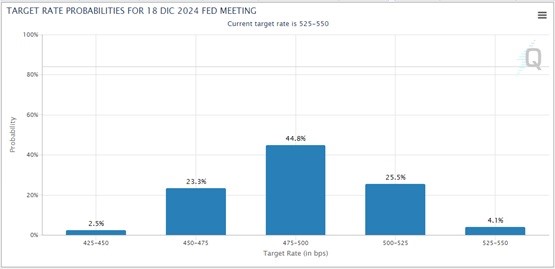

In response to the economic disruptions caused by the COVID-19 pandemic, the Federal Reserve drastically lowered interest rates to near-zero levels in 2020. However, the economic recovery, coupled with persistent inflationary pressures, prompted the Fed to begin raising rates in 2022. As of mid-2024, the Federal Reserve has kept interest rates in the range of 5.25% to 5.50%, with cautious optimism about future reductions contingent on inflation and economic trends.

More recently, as of June 18, Federal Reserve officials are seeking additional confirmation that inflation is easing and monitoring for any warning signs from a robust labor market. They are cautiously moving towards what many anticipate will be one or two interest rate cuts by the end of this year.

Impact on Private Credit Markets: Borrowing Costs & Loan Pricing

Interest rates directly affect the cost of borrowing for private credit funds and their borrowers. Higher interest rates increase the cost of capital for lenders, which in turn makes loans more expensive for borrowers. This can lead to a decrease in loan demand, particularly in interest-sensitive sectors such as consumer finance and real estate. Conversely, lower interest rates reduce borrowing costs, potentially increasing demand for private credit & non-bank lending.

For private lenders like Stratus Financial, which specializes in student loans for pilot training, having variable rates is crucial. Variable rates allow the company to adjust loan pricing in response to changes in the prevailing interest rate environment. These rates are typically tied to a benchmark rate, such as the prime rate or LIBOR, and fluctuate based on market conditions. This mechanism ensures that Stratus can offer competitive loan rates by automatically adjusting to economic changes, balancing the need to maintain attractive returns with the goal of ensuring affordability for borrowers, especially in times of high interest rates.

Investment Returns

Private credit funds seek to deliver superior returns compared to traditional fixed income investments. However, higher interest rates can compress profit margins as the cost of capital increases. To maintain target returns, funds may need to adjust their investment strategies, such as shifting towards higher-yielding but potentially riskier loans.

Despite these challenges, the private credit market offers opportunities for attractive returns. Stratus Financial, for instance, provides double-digit returns (13%) by focusing on super-prime borrowers and niche markets like pilot training. This approach mitigates risk while capitalizing on high-demand sectors.

Economic and Market Conditions

Interest rates are influenced by broader economic and market conditions, including inflation, GDP growth, and employment levels. Persistent inflation has been a significant factor in the Federal Reserve’s decision to maintain higher rates in recent years. Private credit funds must stay attuned to these economic indicators to anticipate rate changes and adjust their strategies accordingly.

STRATEGIC CONSIDERATIONS FOR PRIVATE CREDIT FUNDS

Proactive Interest Rate Monitoring

Private credit funds should establish a proactive approach to monitoring interest rate trends and economic indicators. Tools like the CME Group’s FedWatch can provide valuable insights into market expectations for rate changes. By staying informed, funds can make timely adjustments to their investment and lending strategies.

Interest Rate Caps and Floors

Interest rate caps and floors are financial instruments that help lenders like Stratus Financial manage the risk associated with fluctuating interest rates. These instruments provide a way to set upper and lower limits on the interest rates they pay or receive, offering protection against significant rate movements.

Enhancing Borrower Credit Quality

Maintaining a high standard for borrower credit quality is essential. Stratus Financial’s focus on super-prime and prime borrowers ensures low default rates and stable loan performance. Implementing stringent credit assessment criteria and requiring co-borrowers or additional collateral for subprime borrowers can further enhance portfolio quality.

Asset-Liability Matching

Asset-liability matching is a crucial strategy to hedge against interest rate cuts from the Federal Reserve. This approach involves aligning the interest rate characteristics of the lender’s assets (loans) and liabilities (borrowings or deposits) to mitigate the impact of interest rate fluctuations on the company’s financial health and operations.

CONCLUSION

Interest rates have a profound impact on the private credit space, influencing borrowing costs, investment returns, and overall market dynamics.

For private credit funds like Stratus Financial, navigating the current high-rate environment requires strategic adjustments and proactive risk management. By focusing on high-quality borrowers, diversifying portfolios, and leveraging technology, private credit funds can continue to deliver attractive returns while mitigating the risks associated with interest rate fluctuations.

Understanding and adapting to the complex interplay of interest rates and economic conditions will be key to sustaining growth and success in the private credit market. Stratus Financial’s strategic approach serves as a valuable model for other private credit funds aiming to thrive in an evolving financial landscape.

REFERENCES:

- CME GROUP: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- Cohen, C., Ferreira, C., Natalucci, F., & Sugimoto, N. (2024, April 8). Fast-Growing $2 Trillion Private Credit Market Warrants Closer Watch. IMF. Retrieved from https://www.imf.org/en/Blogs/Articles/2024/04/08/fast-growing-USD2-trillion-private-credit-market-warrants-closer-watch

- Gravier, E. (2024, May 16). How having super-prime credit can save you more than 3X on interest payments. CNBC. Retrieved from https://www.cnbc.com/select/super-prime-credit-definition/

- Moscosamayo, A. (2024, May 2). Fed ‘paraliza’ su tasa de interés por sexta vez: Ve ‘falta de avance’ vs. la inflación. EL FINANCIERO. Retrieved from https://www.elfinanciero.com.mx/economia/2024/05/01/fed-paraliza-su-tasa-de-interes-la-mantiene-sin-cambios-por-sexta-vez-consecutiva/